Designing the SNIPES Wallet

Accrue × SNIPES • 2025–2026

SNIPES — one of the biggest sneaker retailers in Europe and the US — partnered with Accrue on a first-of-its-kind co-branded wallet. When I joined it was pre-launch: built, and ready for its first round of user testing. I ran that testing, redesigned the wallet around what the data showed, then designed the roadmap's must-have features — surface by surface.

Start with the problemSNIPES × Accrue — the wallet launch commercial, featuring Marlon Wayans

Product

SNIPES mobile wallet, Accrue embed SDK

Team

1 Designer (me), 2 PMs, 3 Engineers, 1 QA

Timeline

Apr 2025 – present

Role

Research, strategy, design, testing

THE CLIENT

Accrue × SNIPES

Accrue builds white-label co-branded wallet and loyalty platforms for enterprise retail brands. SNIPES is the flagship. I led design across the whole wallet — how users onboard, fund it, pay in-store, enter sneaker drops, gift to friends, and earn offers.

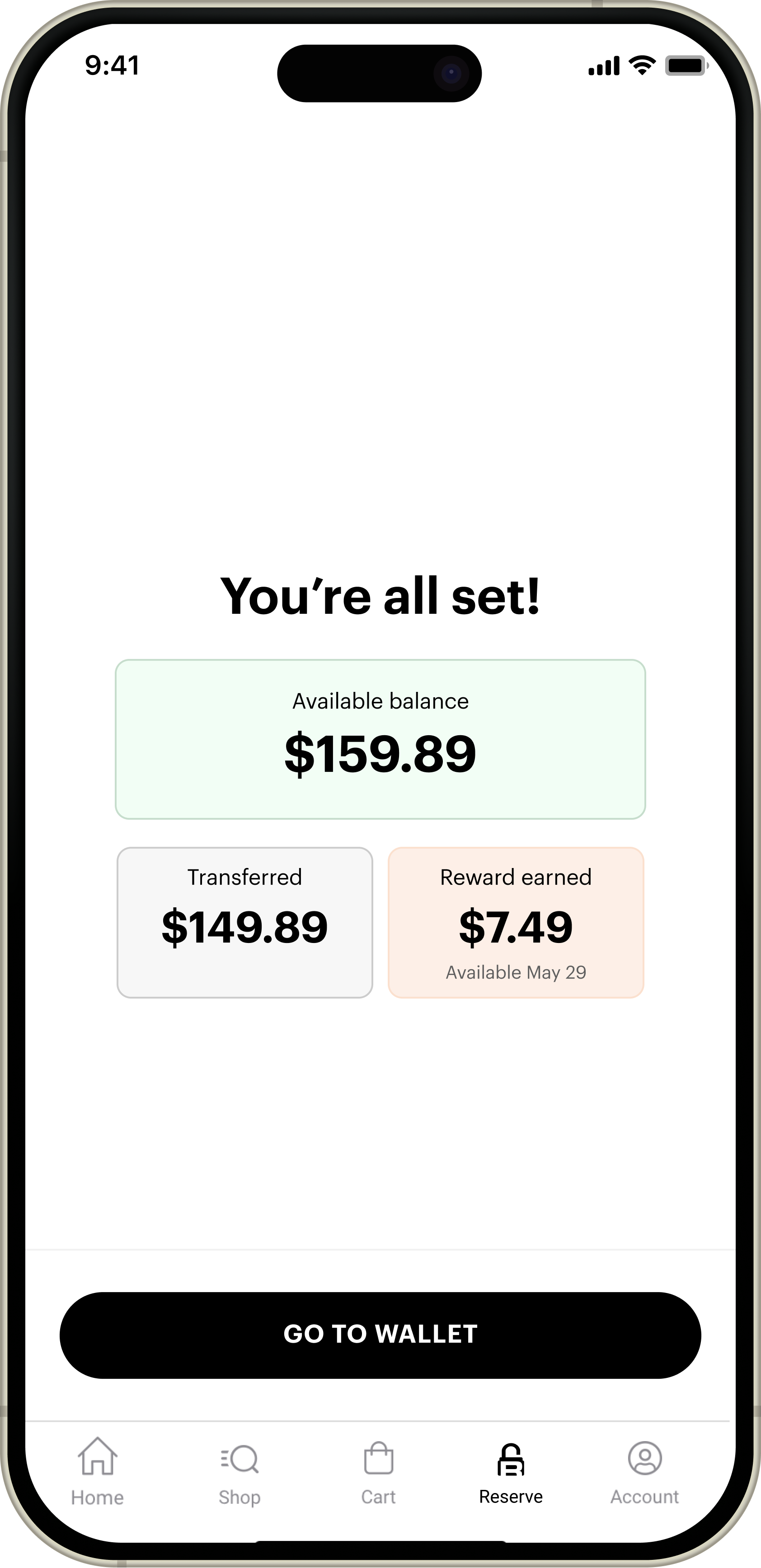

SNIPES partnered with Accrue on a co-branded wallet: pre-load money, pay in-store, and earn cashback for shopping. The bet was that a wallet could turn casual sneaker buyers into repeat customers. When I joined in April 2025 the wallet was built but still pre-launch — designed on instinct, without a single user in the room. My first job was to put it in front of real people and find out what actually worked.

THE CHALLENGE

Why would a sneaker shopper load money into a retailer's wallet before they've bought anything? Every surface I designed had to answer that — and in testing, the early flow was losing more than half of the people who tried it.

PROJECT GOALS

- 1Users: understand what each step is for. → Business: stop the 55.9% KYC drop-off eating new wallets.

- 2Users: pay fast and confidently in-store. → Business: make the wallet the default checkout, not a novelty.

- 3Users: feel real value — cashback, drops, gifts. → Business: drive funding and retention past the profile-completion cliff.

THE PROBLEM

A first-of-its-kind wallet — and a skeptical audience.

Before I designed anything, I had to be honest about what we were up against: a brand-new kind of retail wallet, built pre-launch on instinct, and a genuine question about why anyone would use it at all.

The bet: turn buyers into repeat customers

A co-branded wallet was SNIPES' play to build loyalty — pre-load money, pay in-store, earn cashback. But it asked something unusual up front: put money into a retailer's wallet before you've bought a thing. Testing made the gap obvious — users didn't get the value prop. So the work was cut out for us: tighten the UX and the copy enough to make an already-skeptical shopper actually see the value.

Wallet home / value prop screen

Four surfaces across the user's lifecycle

Onboarding gets people in the door, but the wallet only earns its place across the whole lifecycle — at the register, during a drop, and between friends. The work spanned the four surfaces that matter most to both users and the business: onboarding, scan-and-pay, drops, and gifting — each answering 'why come back' at a different moment.

Map of the four surfaces across the user lifecycle

RESEARCH

I sat with 34 users before I drew a single screen.

A mix of moderated one-on-one sessions and focus groups, 30 minutes each. I put a detailed prototype of the entire early product in front of them and watched where they hesitated, got excited, and got confused.

Study setup: 34 participants, 30-min sessions + focus groups

Who I talked to, and how

Thirty-four sneaker shoppers, ages 18–45, mixed on payment-app comfort and SNIPES familiarity — recruited so no single profile could dominate. Each walked through a detailed prototype of the early product, narrating as they went. No leading questions.

Research question set / discussion guide

The questions I actually asked

I kept them concrete and non-leading, so the friction had to surface itself:

- "What do you think this screen is asking you for?"

- "Would you enter your card here? Why or why not?"

- "What does '5% back' mean to you — in dollars?"

- "What would make you load money now instead of later?"

- "Where do you think you are in this process?"

Synthesis: five themes from 34 sessions

The answers that reset the brief

The pattern was consistent and uncomfortable:

- 'Verify your Identity' read as a credit check — several physically flinched

- Nobody could explain what 'backup payment' was for, so they skipped it

- most couldn't turn '5% back' into a real dollar amount

- Most wanted to explore the app before committing money

- Almost no one knew how many steps were left — the flow felt endless

Users could tell me 'this is confusing' instantly, but never why. So I stopped asking. Where they paused, what they misread, what they skipped — that's what wrote the brief. It's the lens I carried into every surface after onboarding.

WHAT I FOUND

"Verify your identity" made people flinch.

The research pointed at four concrete problems — all of them language and hierarchy, not features. Which is exactly why they were fixable, and why the fixes generalized to every surface after.

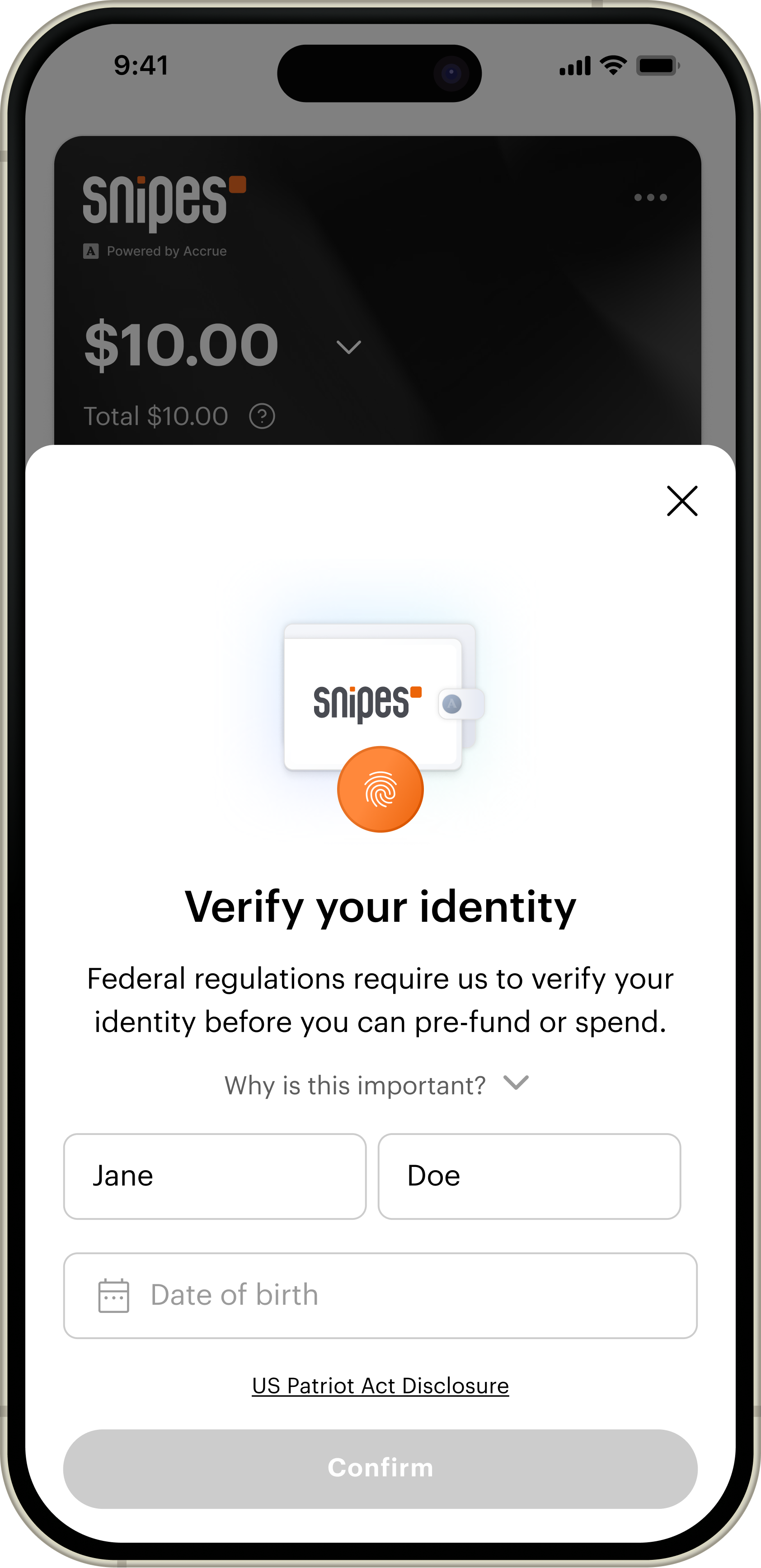

The KYC step read like a government audit

We needed a name, birthday, and address — information people share constantly. But the word 'verify' set off alarms. Several participants physically flinched. We were losing users who'd have handed this over happily in a warmer frame.

KYC bottom sheets: name + birthday, then address

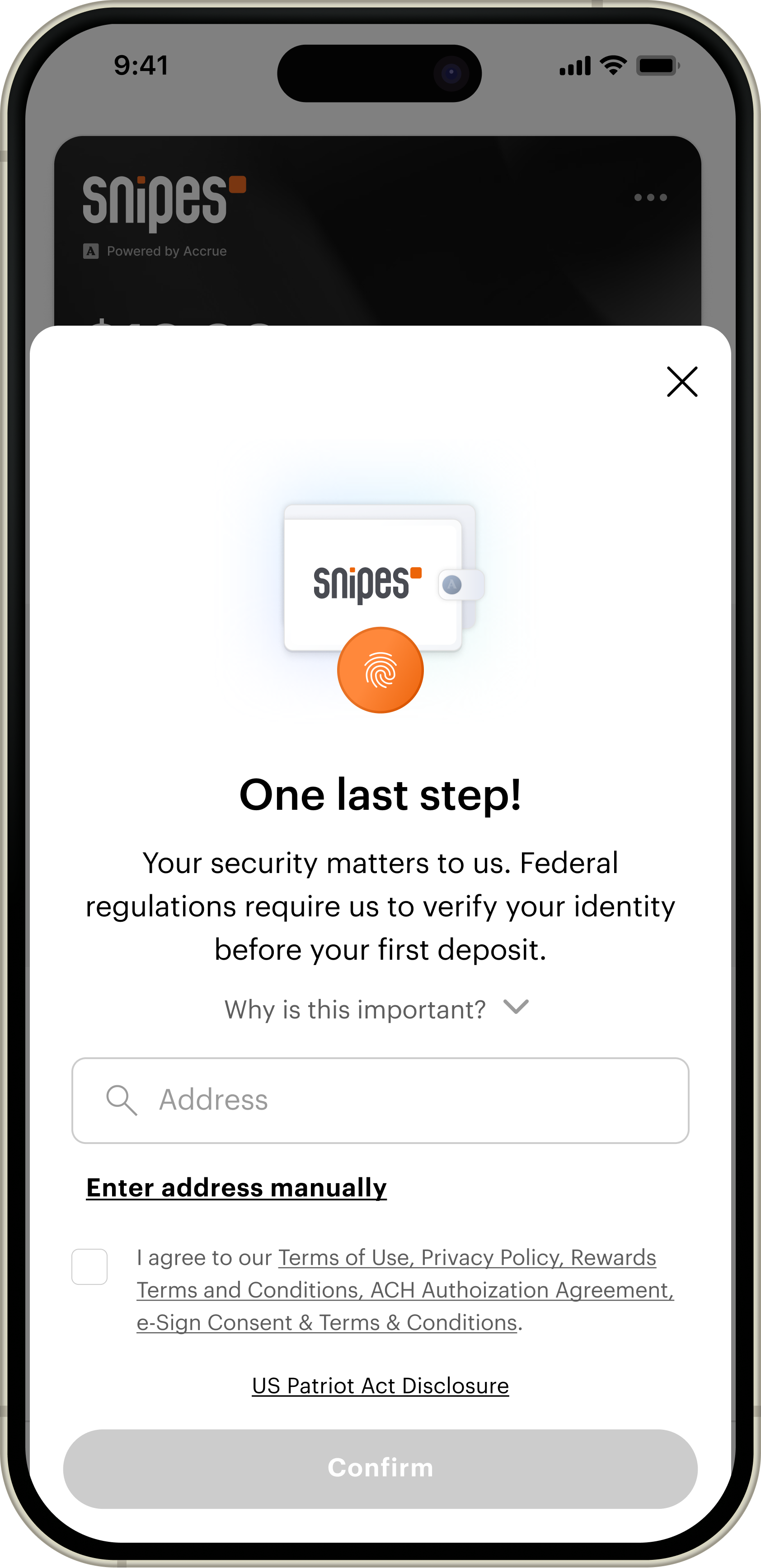

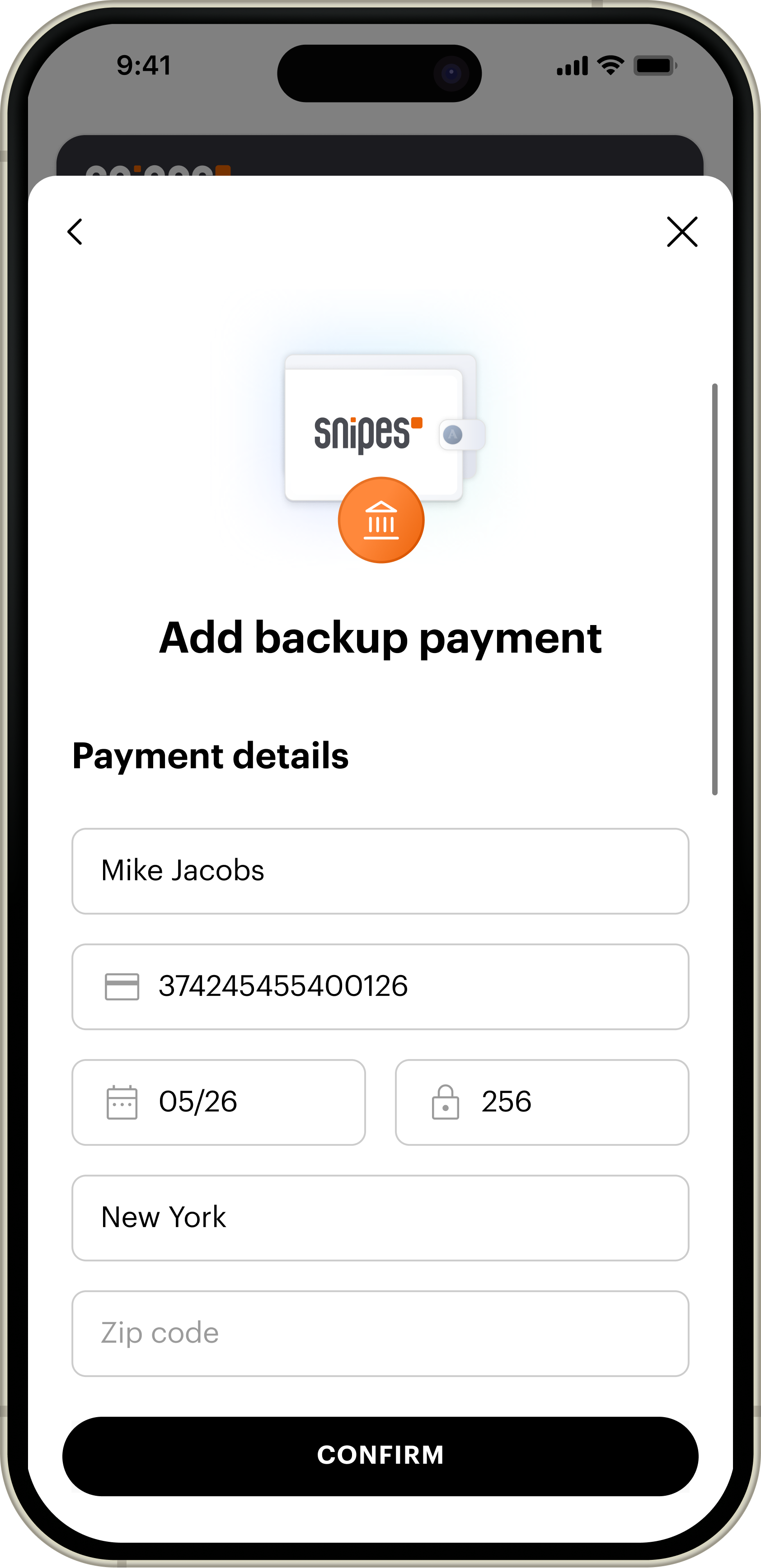

"Backup payment" never said backup for what

The screen asked for card details without explaining why. Participants couldn't articulate what it was for or what would happen to their card, so they skipped it — and skipping it quietly broke the wallet later.

Old 'Add backup payment' form

Percentages didn't land. Dollars did.

Most couldn't connect '5% back' to real money. The actual dollar figure was on the screen — small, under a giant orange 5% hero. Leading with the dollar amount in testing made comprehension instant.

Old reward screen: 5% hero, $1.00 in small body text

Nobody could tell what was mandatory

Bottom sheets read as dismissible notifications. The flow had no visible end. Stalled users got no next step. One put it plainly: 'I already gave you my name, email, and phone.'

Bottom-sheet cascade with no visible end

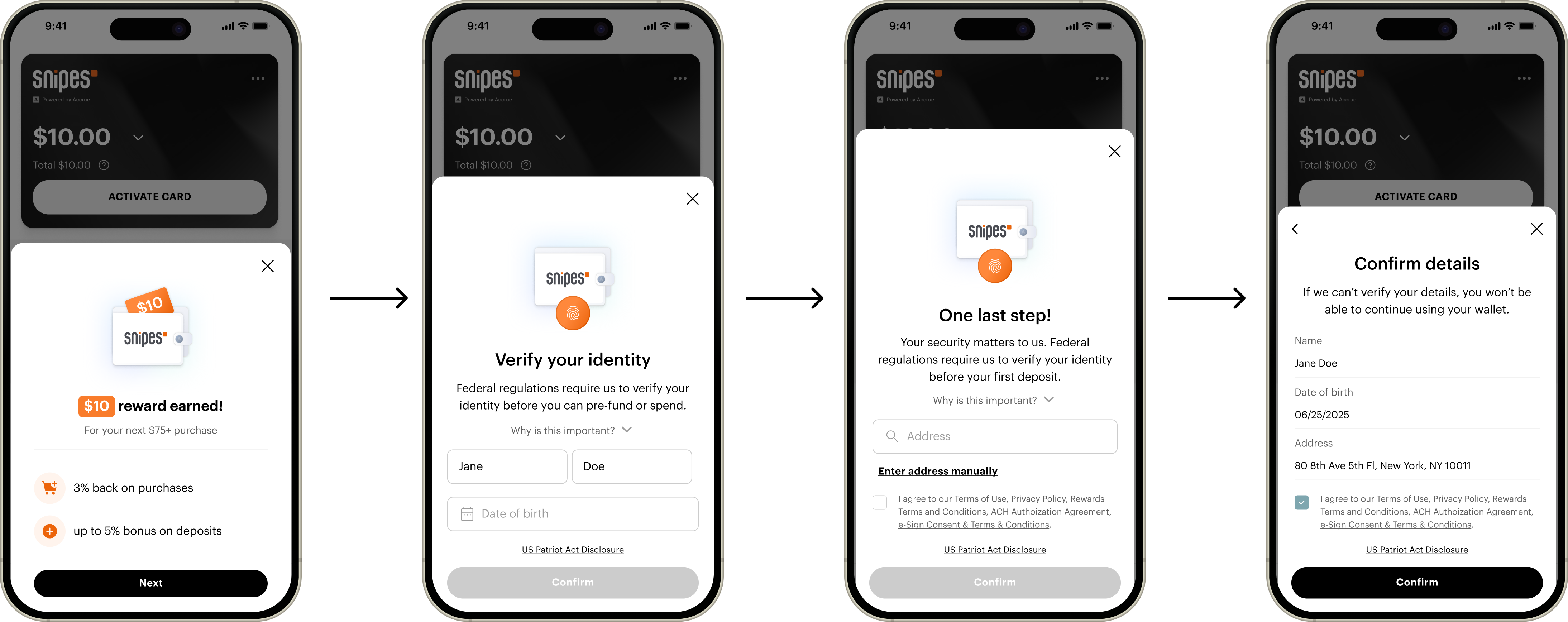

ONBOARDING

Rebuilding the front door around what they said.

Every move below traces to a line from the research. This is the anchor surface — the one with the numbers behind it.

A 3-step stepper, finish line visible from step one

Sign Up → Complete Profile → Set Up Payment. Each step's subtitle says why it matters. The open-ended checklist that surprised people in the study was gone. Profile completion rose 24 points.

3-step stepper with progress indicator

Copy rewritten for skimmers

'Verify your Identity' became 'Set Up Profile.' 'Backup payment' became 'We'll charge this card beyond your balance. You'll earn 3% back on that amount.' Dollars replaced percentages wherever the context allowed.

Drag to compare: '5% back' vs the dollar amount

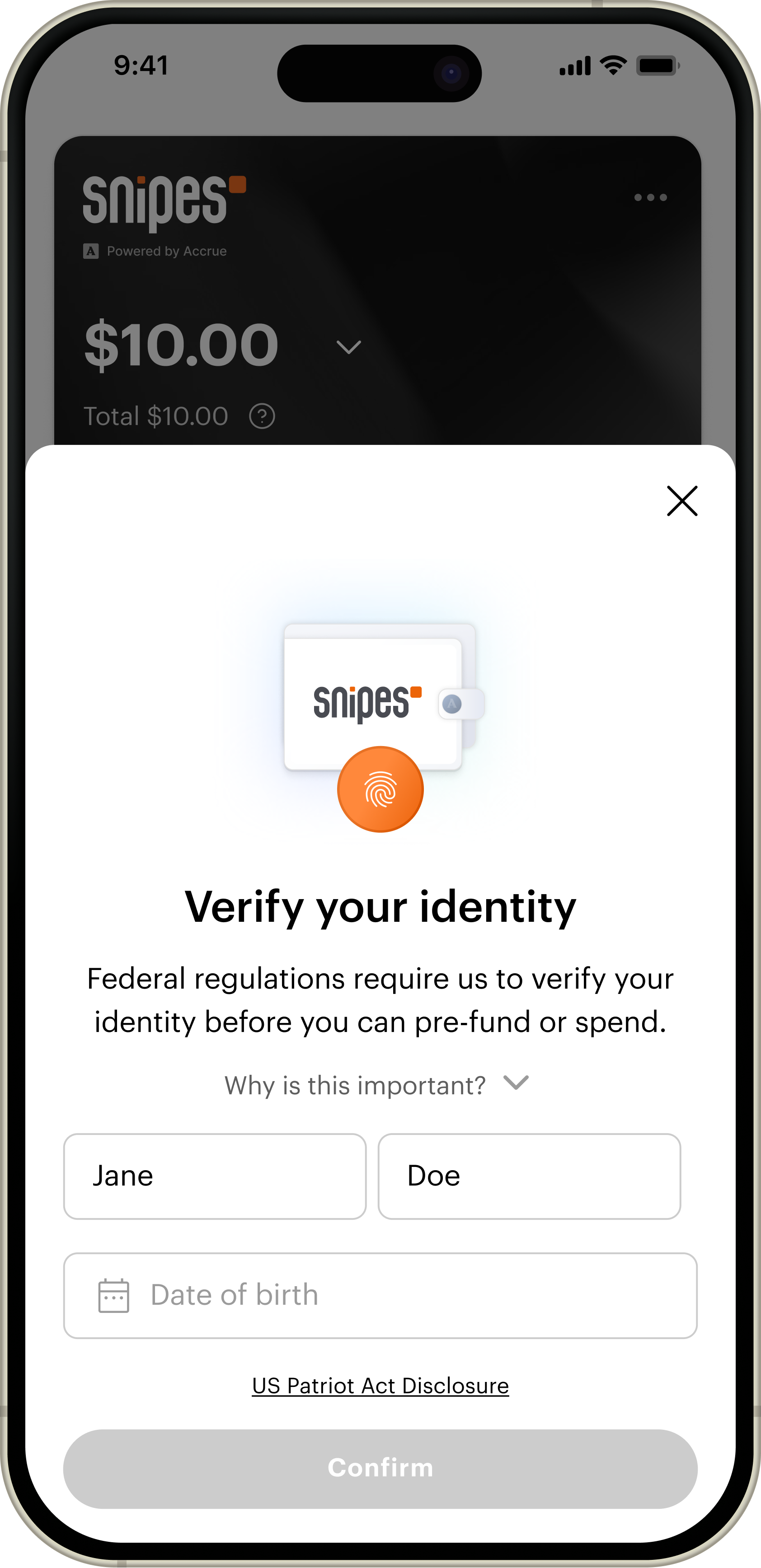

KYC promoted out of a bottom sheet

Moved into a full-screen step inside the stepper. Hierarchy alone signaled importance — no persuasion copy needed. On re-test, users treated it as a real step instead of a swipe-away notification.

KYC: bottom sheet (before) vs full-screen step (after)

Blocking states that tell the truth

Blocked, under review, documents needed — each now explains what happened and gives one clear way forward, instead of leaving stalled users on a dead dashboard.

Blocking states triptych: blocked / review / docs

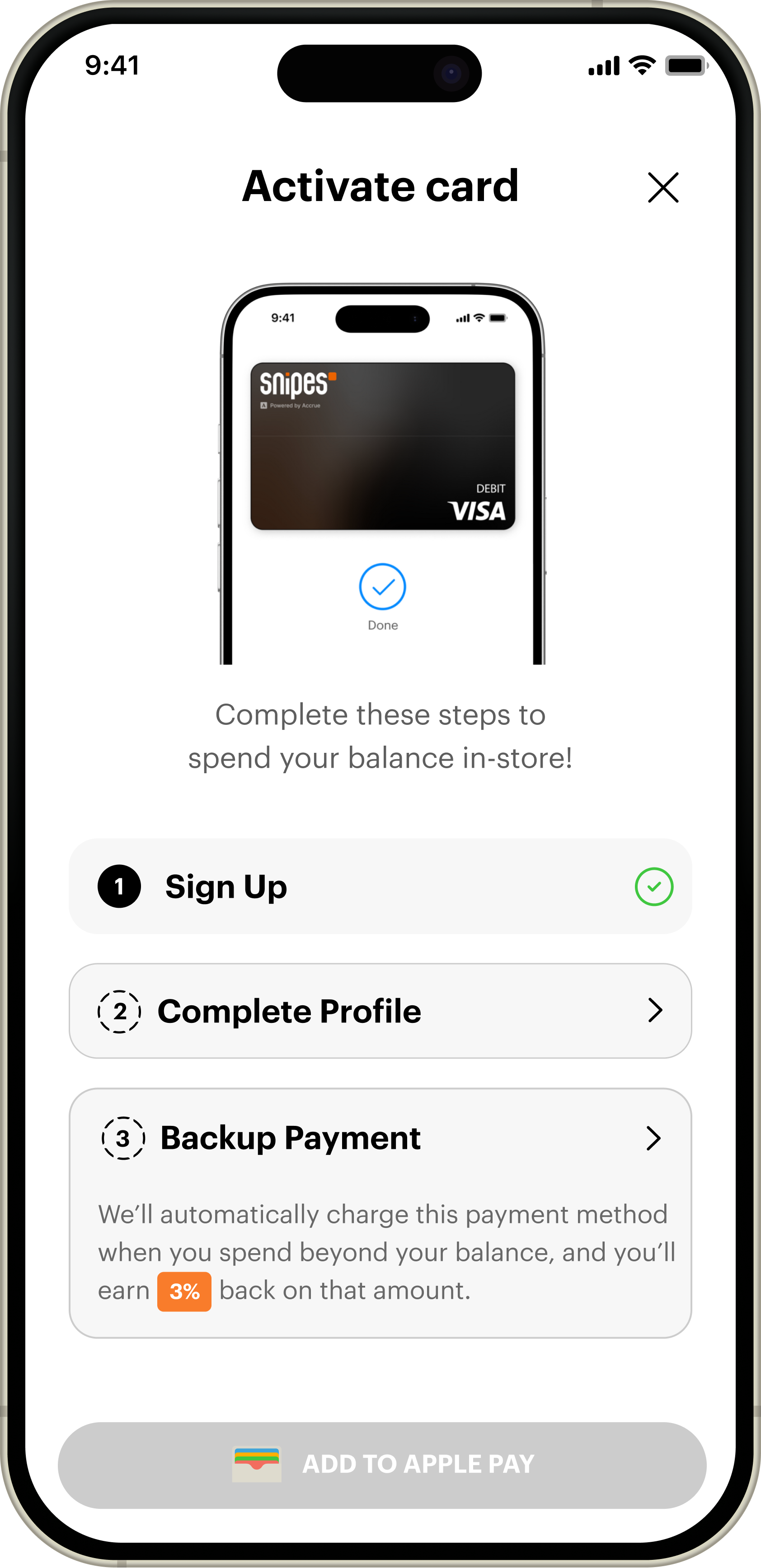

SCAN & PAY

Checkout felt like a leap of faith.

I soft-launched onboarding with 50+ SNIPES employees using the wallet at the register during real shifts. That's where the deepest problem showed up — not in the funnel, but in the two seconds of doubt at the counter.

The user problem: nobody could see what was happening

With tap-to-pay, a customer tapped their phone and… hoped. They couldn't see their balance, couldn't tell if the payment went through, and the clerk couldn't confirm anything on the customer's screen. In a busy store, that two-second doubt sent people straight back to cash or card. The wallet felt riskier than the thing it replaced.

Tap-to-pay moment of doubt at the register

The fix: a barcode both sides can see

Barcode scan-and-pay puts the balance and a scannable code right on the customer's screen. The customer sees their money; the clerk scans and confirms out loud. It solved the user's doubt and the business's broken clerk-interaction in one move — which is why the business made it the checkout model.

Barcode scan-and-pay screen with balance toggle

Cutting entry friction at the counter (exploring)

Manual card entry was slow mid-shift, so I'm exploring camera-based, on-device card scanning to speed it up — keeping card data off the network. Early-stage; not committed yet.

GIF slot — card-scan concept

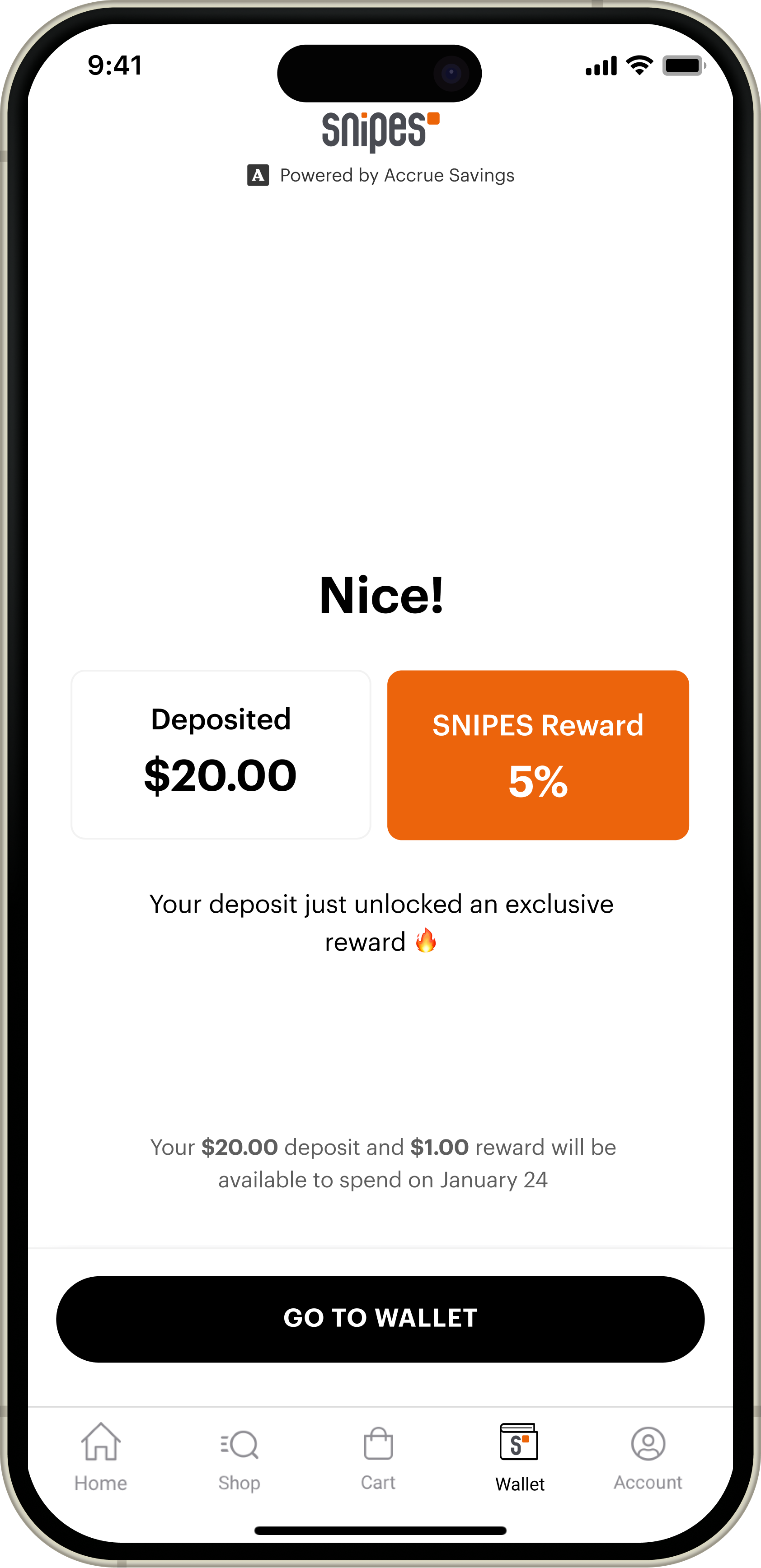

DROPS

SNIPES was losing the drop.

Exclusive sneaker drops are where sneaker culture lives — and where SNIPES was losing customers to competitors. The raffle system was clunky, there was no way to buy a hyped pair in-store, and nothing kept the excitement alive between the announcement and the release. Drops are directly revenue-generating, so this wasn't a nice-to-have. We needed a fix, fast.

The problem: hype with nowhere to go

Competitors had smoother ways to enter drops and reserve pairs. SNIPES customers couldn't reliably buy the shoes they were hyped for, had no in-store path to claim them, and lost interest in the dead air between drop announcement and release. Every one of those gaps was leaking revenue on the brand's most valuable inventory.

GIF slot — the full drops experience

Entering a drop, inside the wallet

The wallet became the place to enter a drop — with Reserve balance improving your odds, so the feature ties straight back to funding, and a clear in-store path to claim a winning pair. (Detailed final flow to be added.)

Drop entry screen with Reserve balance and odds

When you don't win

Most entrants lose, so the emotional design problem is the loss. The 'missed' screen stays honest — you didn't win — but a consolation offer arrives on top of it, framed as a real reward, so a loss still gives the user a reason to stay.

'Missed' loss screen + consolation offer

GIFTING

The most personal way to grow the wallet.

Sneakers are one of the most gifted things there is — birthdays, holidays, a parent staking a teen's next pair. But there was no native way to send that money into SNIPES. This is the surface I'm designing right now: gifting as a growth loop, where every gift can bring a new wallet holder. (Drafted from the current direction — I'll make it exact as the work lands.)

The problem: gifting sneakers is clunky

People hand over cash or a generic gift card and hope it gets spent on the right thing. Neither feels personal, and neither brings anyone into the SNIPES wallet or its rewards. A whole natural moment of demand was going somewhere else.

GIF slot — gifting flow

Send a gift straight into the wallet

Choose an amount, personalize it, and send. The recipient gets notified and redeems it into their SNIPES wallet — which quietly onboards them if they're new, and drops branded balance right where it'll be spent in-store.

Send-a-gift + redeem screens

Why it matters: a growth loop, not a feature

Gifting turns existing users into a channel. Every gift is a reason for someone new to open the wallet, and gifted balance is money that comes back to SNIPES at the register. It's referrals' job — done with something people actually want to send.

Gifting loop diagram

OFFERS

Offers users can actually trust.

Rewards only work if users believe them. Two surfaces carried that: the moment an offer is earned, and the fine print about what qualifies.

The offer-earned moment, framed as a reward

A notification drawer that leads with the amount and the product, not confetti. The information hierarchy does the celebrating — reward states stay distinct from return, cancel, and reversal edge states, which read muted so nothing feels falsely positive.

Offer-earned drawer + edge states

Eligibility rules, made legible

Offers exclude some stores and items. Instead of two buried links, one 'Offer Rules' screen tabs cleanly across eligible stores, eligible items, and ineligible items — so the exception is scannable, not a trap.

Offer Rules tabbed screen: stores / eligible / ineligible

FINAL DESIGNS

The wallet, end to end.

From sign-up to barcode, drops to gifting — every surface designed for clarity, speed, and trust, with a real user behind each decision.

Full-width hero composition of the complete wallet flow

The full journey: onboarding → scan-and-pay → drops → gifting

Barcode screen with balance toggle

Barcode as the checkout destination

Drop consolation offer

A loss that still offers something back

Send-a-gift screen

Gifting — the growth loop I'm building now

Mixpanel before/after funnel overlay across the flow

Every change traces back to a specific user quote or metric

THE IMPACT

+24 pts

Profile completion

41.2% → 65.86% after the stepper and rewritten copy shipped.

−11 pts

KYC drop-off

55.9% → 45% at the step that was losing more than half of all new wallets.

12 → 3

Onboarding steps

A shapeless checklist became a 3-step stepper with the finish line visible from screen one.

18K

Wallets / month

Created on the redesigned flow in the last 30 days.

91–99%

Step retention

Between stepper steps. Navigation stopped being the problem — the remaining cliff is funding.

The shipped onboarding pieces — the 3-step stepper, rewritten copy, and honest blocking states — moved every funnel number they touched. That same playbook now runs across the wallet: in-store scan-and-pay, sneaker drops, gifting, and offers. Each surface is designed to answer the one question onboarding raised — why is this wallet worth it — in the moment it actually matters.

LOOKING BACK

Research first, design second.

A few days with 34 users reordered my entire brief. The biggest problems weren't the ones I'd have prioritized on my own — and the pattern held every time I opened a new surface.

Copy is design.

Renaming 'Verify your Identity' to 'Set Up Profile' changed how users read the step. '$1.50 on this purchase' landed where '5% back' bounced. Across the wallet, copy did more than layout.

Design for the moment, not the model.

The business cared about funding and retention. Users cared about buying sneakers, winning drops, and not looking foolish at the register. Every surface had to serve both at once — and lead with the user's moment.

A clear foundation survives the pivot.

Mid-build, the business swapped tap-to-pay for barcode scan-and-pay. Because the redesign was anchored in real problems, the pivot extended the work instead of restarting it.

WHAT I'D DO DIFFERENTLY

I'd run in-store usability testing before public launch, not after. The office sessions caught the language and structure problems, but the speed-at-the-register and clerk-visibility gaps only surfaced once the employee beta hit the counter. Testing in context earlier would have shaped the barcode pivot before the business had to ask for it.

LOOKING AHEAD

Ship the barcode scan-and-pay flow and the funding nudge aimed at the load-cash cliff, and land gifting — the growth loop I'm designing now. Instrument the newer surfaces (drops, gifting, offers) as granularly as onboarding so I can iterate without another full research round.